Quick Answer

Diversification substantially reduces unsystematic risk (most of the benefit comes from the first several stocks added, then diminishes, with no fixed cutoff) but never systematic risk. Sector rotation shifts weightings toward sectors that have tended to lead in expansion and sectors that have tended to hold up in contraction. Dollar-cost averaging produces a lower average cost than average price whenever prices fluctuate, but does not guarantee a profit. A protective put establishes a downside floor, a covered call caps upside for income while providing only a small premium cushion (not a floor) against declines, a collar combines both, and Regulation T sets initial margin at 50% on new eligible equity purchases.

With strategies (asset allocation) and styles (security selection) in place, portfolio managers use specific techniques to manage risk, enhance returns, and maintain discipline. These are the tactical tools in the adviser's toolkit.

Diversification

Diversification is the practice of spreading investments across different asset classes, sectors, geographies, and individual securities to reduce risk.

- Reduces unsystematic (company-specific) risk: the risk that a single company or sector will drag down the portfolio

- Does NOT eliminate systematic (market) risk: the risk that affects all securities (recessions, interest rate changes, inflation)

- Most of the available risk reduction comes from the first several stocks added across different sectors, with diminishing benefit after that; there is no fixed cutoff or consensus number

- Beyond that point, additional stocks provide diminishing risk reduction benefits

- Over-diversification can dilute returns and increase costs without meaningful additional risk reduction

Think of it this way: Diversification protects you from bad luck with a single company (unsystematic risk). But it cannot protect you from a broad market downturn that drags everything down (systematic risk). You can spread your eggs across 100 baskets, but if a flood hits the whole warehouse, every basket gets wet.

Exam Tip: Gotchas

Diversification substantially reduces unsystematic risk but NOT systematic risk. No matter how many securities you hold, you cannot diversify away market risk.

Sector Rotation

Sector rotation is the technique of shifting portfolio weightings among industry sectors based on where you are in the economic cycle. Different sectors have tended to perform better at different stages.

| Economic Stage | Sectors That Tend to Lead | Why |

|---|---|---|

| Expansion | Technology, consumer discretionary, financials, industrials | Consumer spending and business investment are strong |

| Contraction | Utilities, healthcare, consumer staples | People still need electricity, medicine, and food regardless of the economy |

- Cyclical sectors rise and fall with the economy (technology, consumer discretionary, industrials)

- Defensive sectors remain relatively stable regardless of economic conditions (utilities, healthcare, consumer staples)

- Requires accurate economic forecasting; getting the timing wrong can hurt returns

- Often used as a component of tactical asset allocation

Exam Tip: Gotchas

"Defensive" sectors are NOT defense/military companies. Defensive means the sector's performance is relatively unaffected by economic cycles because it provides essential goods and services.

Dollar-Cost Averaging

Dollar-cost averaging (DCA) is the technique of investing a fixed dollar amount at regular intervals regardless of market price.

How it works:

Shares purchased each period = fixed investment ÷ price per share

| Month | Investment | Price/Share | Shares Bought |

|---|---|---|---|

| January | $500 | $50 | 10 |

| February | $500 | $25 | 20 |

| March | $500 | $50 | 10 |

| Total | $1,500 | Avg price: $41.67 | 40 shares |

- Average price per share: ($50 + $25 + $50) / 3 = $41.67

- Average cost per share: $1,500 / 40 shares = $37.50

- The average cost ($37.50) is lower than the average price ($41.67) because the price fluctuated across the three months

Why it works:

- Fixed dollar amounts buy more shares when prices are low and fewer shares when prices are high

- This mathematical relationship (harmonic mean vs. arithmetic mean) makes the average cost lower than the average price whenever prices fluctuate; if the price stayed flat the whole period, the two would be equal

- Can reduce emotion-driven timing decisions by enforcing a disciplined approach

- Reduces the impact of market timing

Think of it this way: Because you invest the same dollar amount each time, your money automatically buys more shares when prices drop and fewer when prices rise. Over time, this pulls your average cost below the average market price.

Limitations:

- Does NOT guarantee a profit or protect against loss

- If the market declines consistently, the investor will still lose money

- In a consistently rising market, lump-sum investing typically outperforms DCA

Exam Tip: Gotchas

Dollar-cost averaging results in a lower average cost per share than the average market price during the investment period, whenever the price fluctuates. However, it does NOT guarantee a profit. If the market consistently declines, the investor will still lose money.

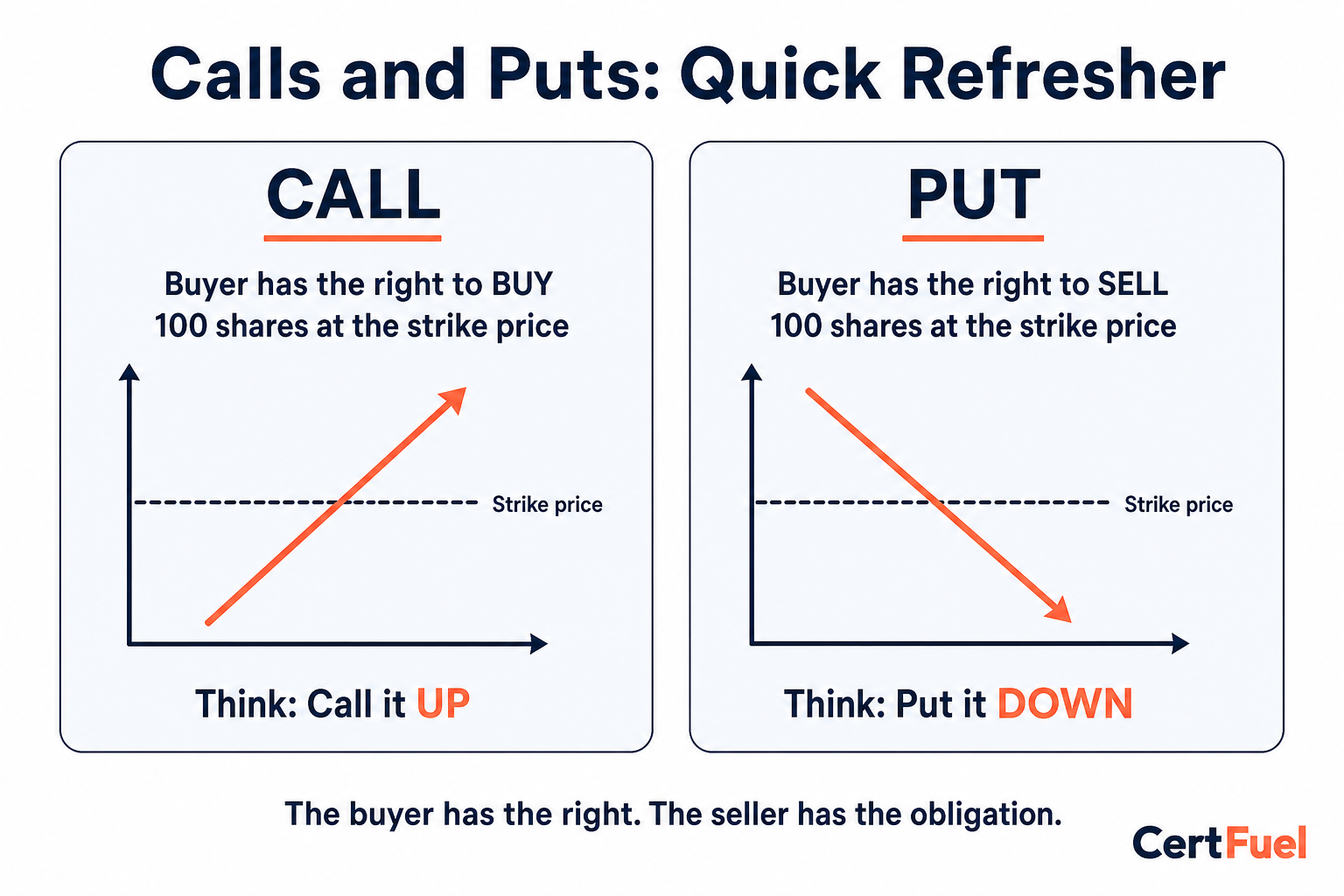

Options as Portfolio Techniques

Options can be used not just for speculation but as practical portfolio management tools. A quick refresher: a standard equity call is the right to buy 100 shares at the strike price, and a put is the right to sell them (adjusted or index/cash-settled contracts can differ). See Options for the full breakdown of calls, puts, premiums, and strike prices.

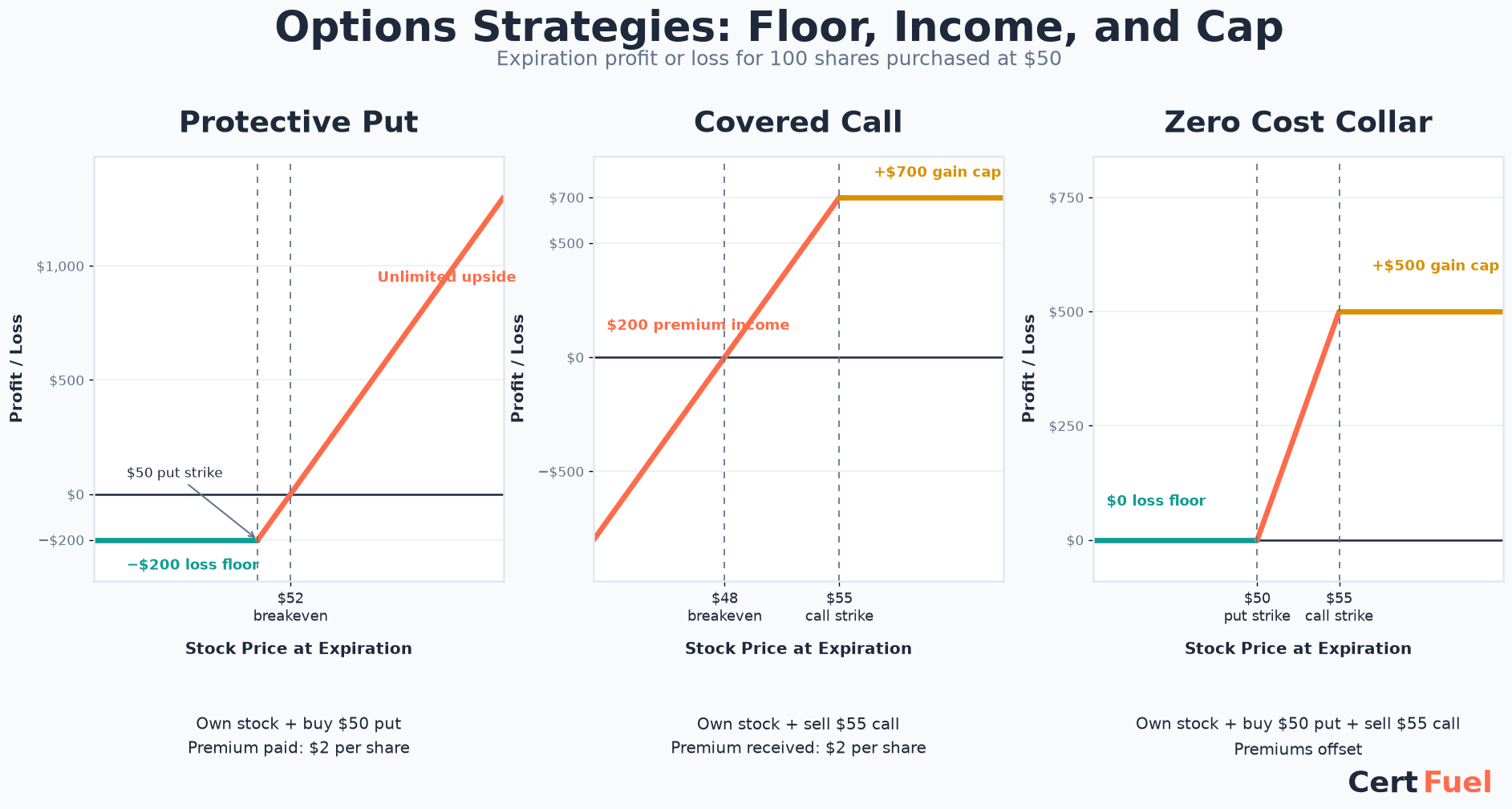

Protective Put

- What: Buying a put option on a stock you already own

- Purpose: Limits downside risk (acts as insurance)

- How: If the stock drops below the put's strike price, you can sell at the strike price instead of the lower market price

- Cost: You pay the put premium, which reduces your overall return

- Best for: Investors who want to hold a stock but protect against a significant decline

Covered Call

- What: Selling (writing) a call option on a stock you already own

- Purpose: Generates income from the option premium

- Trade-off: Limits your upside potential. If the stock rises above the strike price, the call is in the money and assignment should be expected (though not guaranteed), requiring you to sell at the strike price

- Best for: Investors in flat or slightly bullish markets who want extra income

Collar

- What: Combining a protective put AND a covered call on the same stock

- Purpose: Limits both downside and upside. The stock is "collared" between two strike prices

- How: The premium received from selling the call helps offset (or fully covers) the cost of buying the put

- Zero-cost collar: When the call premium exactly equals the put premium, providing downside protection at no net cost

- Best for: Investors who want protection and are willing to cap their gains to get it

| Strategy | Position | Downside Protection | Upside Potential | Net Cost |

|---|---|---|---|---|

| Protective put | Own stock + buy put | Yes, a firm floor (limited to put strike) | Unlimited (minus premium paid) | Premium paid |

| Covered call | Own stock + sell call | Small cushion only (premium received), no floor | Capped at call strike | Premium received |

| Collar | Own stock + buy put + sell call | Yes, a firm floor (limited to put strike) | Capped at call strike | Reduced or zero |

Payoff Shapes at a Glance

The diagram uses 100 shares purchased at $50, a $50 protective put costing $2 per share, and a $55 covered call paying $2 per share. In the zero cost collar, the call premium offsets the put premium.

Exam Tip: Gotchas

A collar limits both upside AND downside. The investor gives up unlimited gains in exchange for a downside floor. A covered call alone provides only a small premium cushion, not a downside floor; the stock can still fall well below where the premium offsets the loss.

Leveraging

Leveraging means using borrowed funds (margin) to increase the size of an investment position.

- Amplifies both gains and losses; margin interest and any change in the loan balance make the net amplification less than perfectly symmetric

- Subject to Regulation T: initial margin requirement of 50% on a new eligible equity purchase in a standard margin account (you must put up at least half the purchase price in cash or qualifying securities; portfolio-margin accounts follow separate rules)

- Maintenance margin: for a long margin equity position, you must generally maintain at least 25% equity after purchase (FINRA minimum; brokers can require more). Short positions, other security types, and portfolio-margin accounts have different requirements

- Margin interest is a cost that must be overcome before earning a profit

- Suitability depends on the client's full profile (resources, objectives, time horizon, liquidity needs, experience, risk tolerance); low risk tolerance is a strong reason margin will generally be unsuitable

Example: With $10,000 in cash and 50% margin, you can buy $20,000 worth of securities.

- If the investment rises 10%: You gain $2,000 on your $10,000 cash (20% return)

- If the investment falls 10%: You lose $2,000 on your $10,000 cash (20% loss)

- Plus you owe margin interest regardless of performance

Think of it this way: Leverage magnifies everything. A 10% move in either direction becomes a 20% move on your actual cash. The borrowed money does not care whether you made or lost money; you still owe interest on it.

Exam Tip: Gotchas

Reg T sets the initial margin at 50% for a new eligible equity purchase in a standard margin account. Brokers can set it higher but not lower. A common mix-up is confusing the 50% initial margin (Reg T) with the 25% maintenance margin on a long margin equity position (FINRA minimum). These are different rules from different regulators, and short positions and portfolio-margin accounts carry different requirements.

Volatility Management

Volatility management encompasses strategies designed to reduce the overall price fluctuations in a portfolio.

- Diversification: The primary tool, spreading across asset classes and sectors

- Hedging with options: Protective puts and collars limit downside volatility

- Alternative assets: Adding assets with low correlation to stocks (real estate, commodities) can reduce overall portfolio volatility

- Volatility-targeting approaches: Dynamically adjusting equity exposure based on current market volatility levels

- Low-volatility investing: Selecting stocks with historically lower price fluctuations. Research shows these stocks often deliver competitive risk-adjusted returns

What Should You Check on Exam Day?

- Diversification substantially reduces unsystematic (company-specific) risk but never eliminates systematic (market) risk, no matter how many securities you hold; most of the benefit comes early, then diminishes, with no fixed cutoff.

- Sector rotation shifts weightings toward sectors that have tended to lead (technology, consumer discretionary, industrials) in expansion and sectors that have tended to hold up (utilities, healthcare, consumer staples) in contraction.

- Dollar-cost averaging produces a lower average cost per share than the average price per share whenever prices fluctuate, but it does not guarantee a profit or protect against loss.

- A protective put establishes a downside floor while leaving upside open (minus the premium); a covered call generates income but provides only a small premium cushion, not a floor, against declines; a collar caps both sides.

- Leveraging amplifies both gains and losses and is subject to Regulation T's 50% initial margin requirement on new eligible equity purchases in a standard margin account; margin interest must be overcome before a position turns a profit; suitability depends on the client's full profile, with low risk tolerance a strong reason against it.